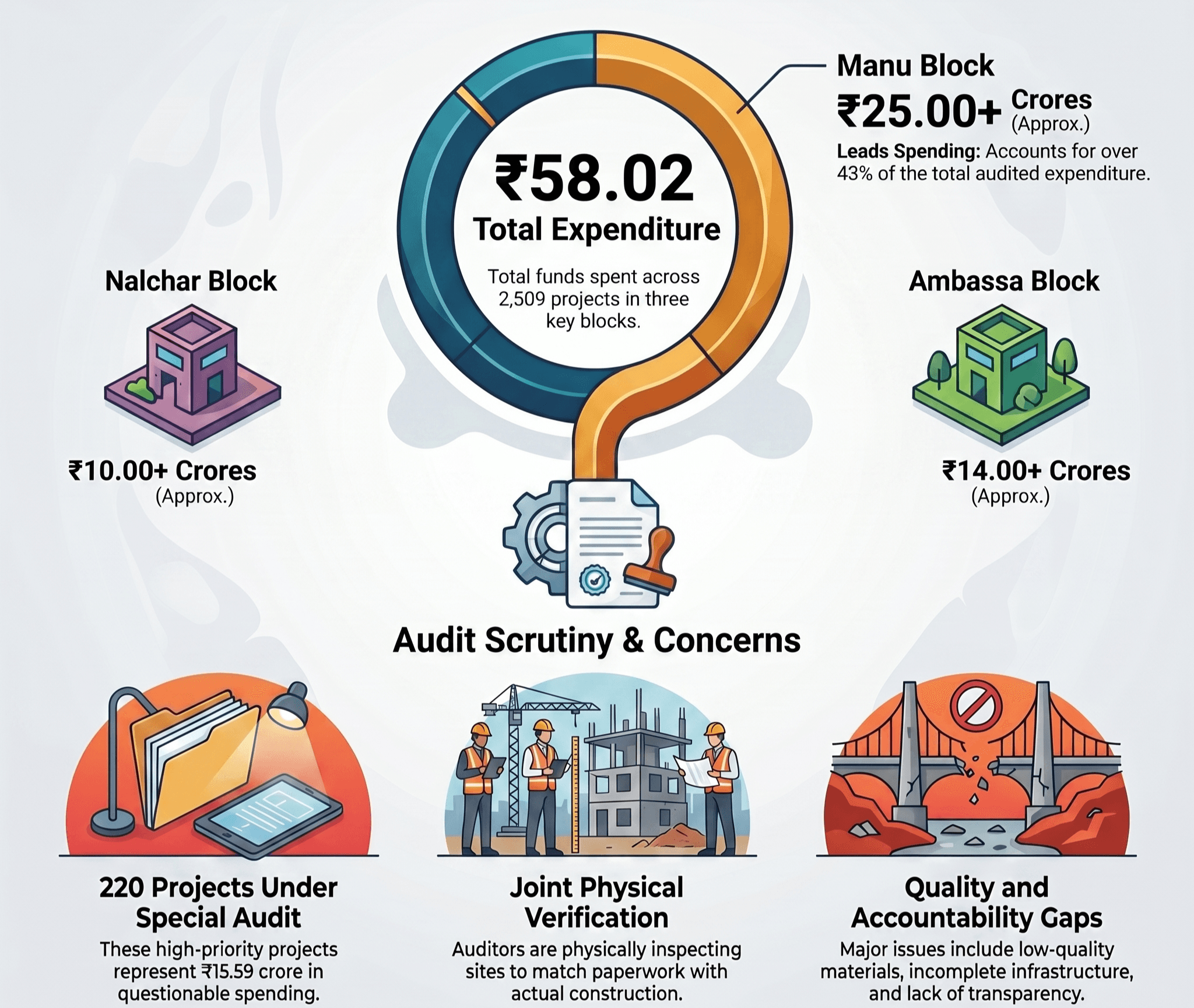

CAG Report Raises Questions Over Fund Management in Tripura's Rural Development Sector

The report has also intensified questions regarding accountability. Critics ask what action, if any, has been taken against officials responsible for the delays identified by the CAG. They also question why details regarding responsibility and corrective measures have not been made public.

A recent audit report by the Comptroller and Auditor General (CAG) of India has brought to light serious concerns regarding the management of development funds in Tripura, placing the State's Rural Development and Finance Departments under scrutiny.

The findings, contained in the CAG's Audit Report for 2023-24, present a troubling picture behind the government's claims of development and administrative efficiency. According to the report, substantial funds sanctioned by both the Central and State Governments between the financial years 2019-20 and 2023-24 were not transferred to the designated Single Nodal Agency (SNA) accounts within the prescribed timeframe.

The report notes that more than ₹1,835 crore was allocated during this period for the implementation of various development projects. However, repeated delays were observed in the release and deposit of these funds, raising questions about administrative efficiency and financial management.

The audit findings have triggered debate over responsibility for the delays. Questions are being raised about whether the lapses originated within the Rural Development Department, the Finance Department, or among senior officials involved in project implementation. Observers argue that if funds earmarked for public development do not reach project accounts on time, claims of rapid development lose credibility.

According to the CAG report, during the financial year 2019-20, several instalments of Central funds experienced delays ranging from two to twenty-one days before being credited to SNA accounts. These allocations included ₹533.24 lakh, ₹643.21 lakh, ₹196.15 lakh and ₹359.98 lakh. Similar delays were also recorded in the transfer of the State's matching share, indicating administrative shortcomings at an early stage.

The situation showed little improvement in 2020-21. The audit identified delays of up to nine days in the release of major allocations, including ₹6,378.08 lakh and ₹507.50 lakh. Funds intended to support development projects reportedly remained tied up in administrative procedures instead of reaching implementation agencies on schedule.

The most significant delay was recorded during the financial year 2022-23. According to the audit, a Central allocation of ₹3,661.45 lakh took twenty-seven days to reach the SNA account. The report describes this as a serious administrative lapse, particularly when funds were intended to support rural roads, drainage systems, water conservation projects, employment generation initiatives and infrastructure development.

The pattern continued in 2023-24. The audit found that the transfer of ₹6,946.17 lakh from the Central Government and ₹2,315.56 lakh from the State Government to the SNA account was delayed by four days. While four days may appear minor in isolation, experts note that repeated delays over several years point to systemic weaknesses rather than isolated incidents.

Economists argue that delays in fund releases affect far more than accounting procedures. They can slow project execution, delay wage payments, hamper construction activities and negatively impact local economies. Rural development programmes, in particular, rely on a steady flow of funds, and interruptions can directly affect farmers, labourers, small businesses and rural communities.

The report has also intensified questions regarding accountability. Critics ask what action, if any, has been taken against officials responsible for the delays identified by the CAG. They also question why details regarding responsibility and corrective measures have not been made public.

Observers point out that announcing development projects worth hundreds of crores is only one part of governance; ensuring that funds reach projects on time is equally important. The audit findings suggest that weaknesses within the administrative framework may be slowing the pace of development despite significant financial allocations.

As the CAG is India's highest constitutional audit institution, its observations carry substantial significance. The report is not a political document but an official audit record. Therefore, experts argue that the findings warrant serious attention rather than dismissal.

With repeated delays in transferring Central and State funds between 2019-20 and 2023-24 now officially documented, public attention is increasingly focused on the effectiveness of Tripura's financial and administrative systems. Many are asking whether development targets can be achieved if allocated funds do not reach project accounts on time.

The audit findings have renewed calls for greater transparency, accountability and administrative reforms to ensure that development funds are utilised efficiently and reach intended beneficiaries without delay.